Your Complete Guide to the FHA Streamline Refinance in Urbandale, IA

What is an FHA Streamline Refinance?

If you currently have an FHA loan, an FHA Streamline Refinance could be your fastest path to a lower mortgage payment. Also known simply as an FHA Streamline or FHA Streamline Refi, this program is designed to help homeowners in Urbandale, IA, and across Iowa reduce their interest rates quickly and easily.

Unlike a traditional rate and term refinance, the FHA Streamline requires significantly less paperwork. In many cases, there is no appraisal required, and income verification is minimal. If you are a veteran exploring options, you might also want to compare this to the VA Interest Rate Reduction Refinance Loan (IRRRL) if you have a VA loan, but for FHA borrowers, the streamline program is unmatched in its simplicity.

At The Tyler Osby Team at Fairway Independent Mortgage, we are experts at providing second opinions on FHA streamline refinance options. We want to ensure you are getting the best possible terms for your financial future.

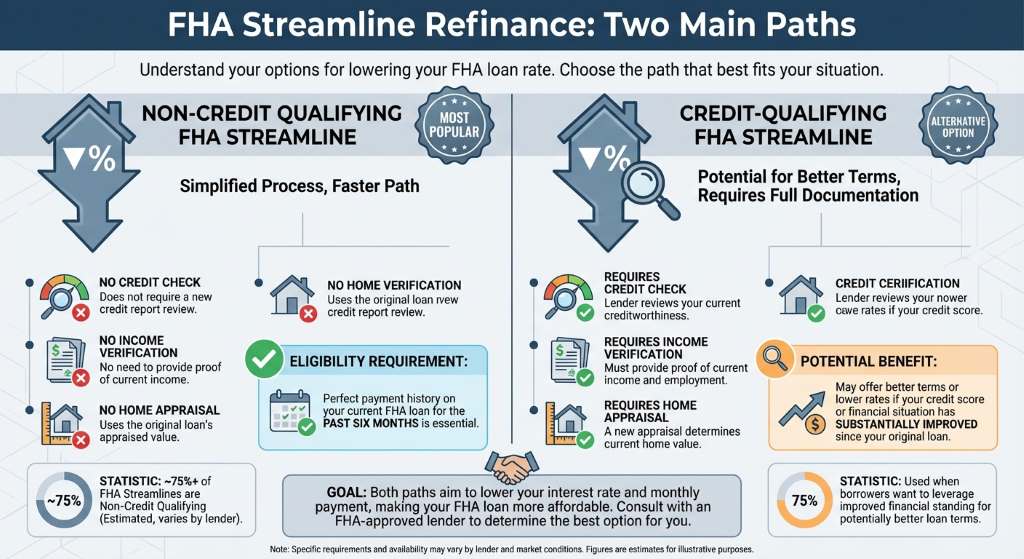

Credit-Qualifying vs. Non-Credit Qualifying FHA Streamlines

When exploring an FHA Streamline Refinance, it is important to understand that there are two main paths you can take: non-credit qualifying and credit-qualifying.

- Non-Credit Qualifying FHA Streamline: This is the most popular option. It does not require a new credit check, income verification, or a home appraisal. As long as you have a perfect payment history on your current FHA loan for the past six months, you may be eligible to lower your rate.

- Credit-Qualifying FHA Streamline: This route requires the lender to pull your credit and verify your income. You might choose a credit-qualifying refinance if you are removing a borrower from the mortgage, such as in the case of a divorce, and the remaining borrower needs to prove they can afford the payments on their own.

Both options offer excellent benefits, but selecting the right one depends on your unique circumstances. Our Urbandale based team can help you navigate these choices effortlessly.

| Feature | Non-Credit Qualifying | Credit-Qualifying |

|---|---|---|

| Credit Check Required | No | Yes |

| Income Verification | No | Yes |

| Appraisal Needed | Typically No | Typically No |

| Best For | Lowering rate quickly with minimal paperwork | Removing a borrower from the loan |

Why Choose The Tyler Osby Team for Your FHA Streamline Refi?

Refinancing your home is a major financial decision. That is why working with a highly recommended local mortgage lender in Iowa is crucial. The Tyler Osby Team at Fairway Independent Mortgage has helped countless homeowners in Urbandale and beyond secure favorable loan terms. We pride ourselves on our transparency, weekly updates, and deep understanding of FHA loans.

Remember, we are experts at providing second opinions on FHA streamline refinance quotes. If another lender has given you an estimate, let us take a look. We might be able to find better terms or point out hidden fees.

Legal Licensing Information: Fairway Independent Mortgage Corporation, NMLS #2289. Tyler Osby, NMLS #8668, State of Iowa License #19545.

Q1: What are the primary requirements for an FHA Streamline Refinance?

You must currently have an FHA loan, have a perfect payment history for the last six months, and the refinance must result in a net tangible benefit, such as a lower monthly payment.

Q2: Do I need an appraisal for an FHA Streamline Refi?

In most non-credit qualifying FHA Streamline scenarios, a new home appraisal is not required. This saves you both time and money upfront.

Q3: Can I get cash out with an FHA Streamline?

No, the FHA Streamline Refinance program does not allow for cash out. If you need to tap into your home equity, you would need to explore a standard FHA cash out refinance.

Q4: How long does the FHA Streamline process take?

Because there is significantly less paperwork and no appraisal required in most cases, an FHA Streamline can often close faster than a traditional refinance, typically within 30 to 45 days.

Q5: Can I add or remove a borrower during this process?

Yes, you can remove a borrower, but doing so usually requires a credit-qualifying FHA Streamline to ensure the remaining borrower can afford the mortgage. Adding a borrower is also possible under specific FHA guidelines.Apply Online with The Tyler Osby Team Today