The 2026 Texas Renewal Wave: Advanced Refinancing Strategies to Protect Cash Flow

Understanding the 2026 Mortgage Renewal Wave

As we approach 2026, many homeowners are bracing for a significant financial shift known as the Texas Renewal Wave. This phenomenon refers to the large volume of adjustable-rate mortgages and interest-only loans originated in previous years that are scheduled to reset or renew. For homeowners, this can mean a sudden and substantial increase in monthly payments, threatening overall cash flow and financial stability.

To navigate this complex landscape, proactive planning is essential. Whether you own property in the Lone Star State or you are looking for expert guidance from a top-rated Urbandale, IA mortgage broker, understanding your options now can save you thousands later. Advanced scenario modeling allows homeowners to compare their current trajectory against potential refinancing strategies.

- Evaluate current loan terms: Know exactly when your rate is set to adjust.

- Assess cash flow impact: Calculate the exact dollar amount your payment might increase.

- Explore early refinancing: Lock in stability before the market becomes saturated with renewal applications.

The Tyler Osby Team at Fairway Independent Mortgage specializes in helping clients build resilient financial strategies to protect their home investments, ensuring peace of mind regardless of market volatility.

Scenario Modeling: Blended Rates and Breakeven Analysis

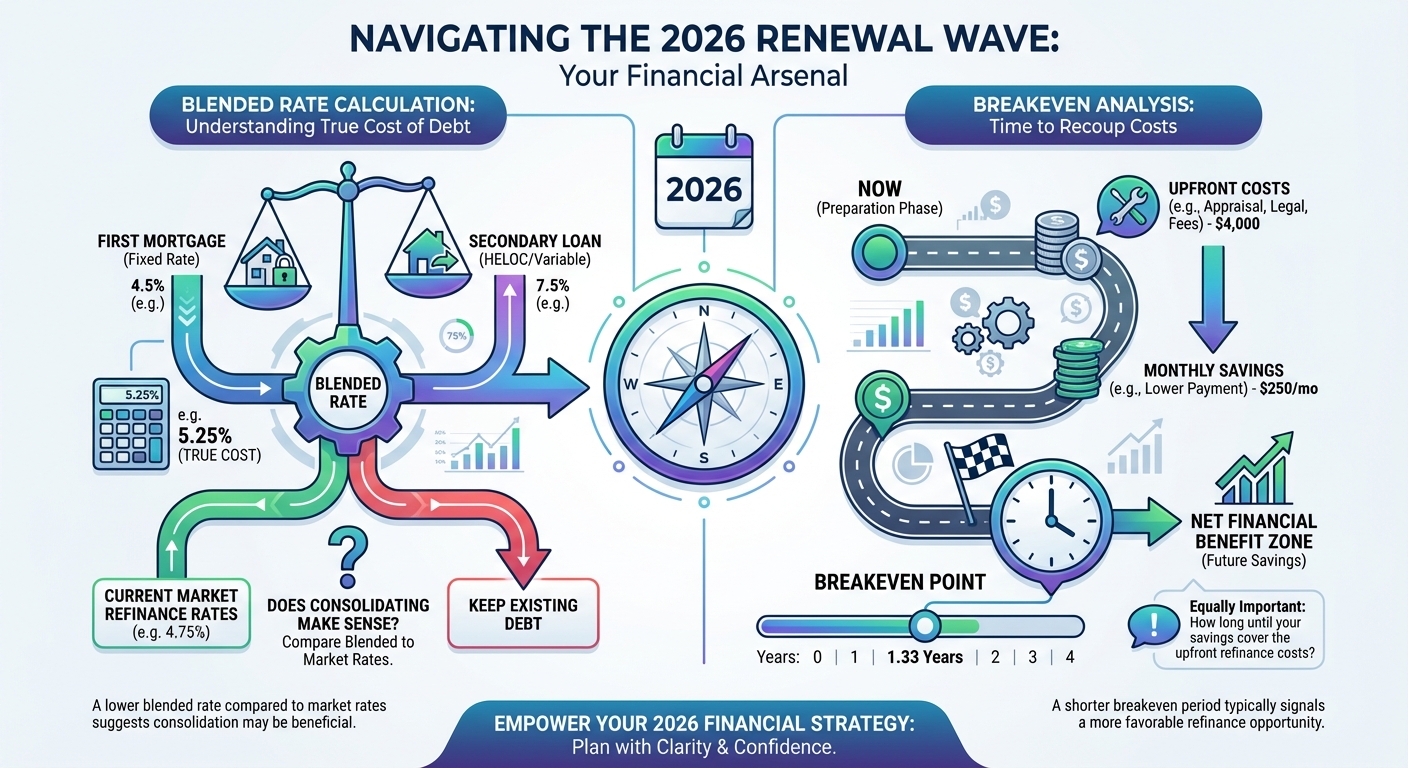

When preparing for the 2026 renewal wave, two of the most powerful tools in your financial arsenal are blended rate calculations and breakeven analysis. A blended rate helps you understand the true cost of your debt if you currently have a first mortgage and a secondary loan, such as a Home Equity Line of Credit (HELOC). By comparing your blended rate to current market refinance rates, you can determine if consolidating your debt makes financial sense.

Equally important is the breakeven analysis. This calculation reveals exactly how many months it will take for your monthly refinancing savings to cover the closing costs of the new loan. If you plan to stay in your home well past the breakeven point, refinancing is typically a smart move to protect your long-term cash flow.

Working with an experienced professional like Tyler Osby, Iowa’s most recommended mortgage lender, ensures these calculations are precise. Here is a look at how different scenarios might play out:

| Loan Scenario | Interest Rate | Monthly Payment | Estimated Closing Costs | Breakeven Point (Months) |

|---|---|---|---|---|

| Current ARM (Resetting) | 7.25% | $2,850 | $0 | N/A |

| Refinance Option A (30-Year Fixed) | 6.125% | $2,430 | $4,200 | 10 Months |

| Refinance Option B (15-Year Fixed) | 5.75% | $3,100 | $3,800 | Immediate Equity Gain |

Optimal Timing Strategies for Homeowners

Timing the market perfectly is nearly impossible, but strategically positioning yourself ahead of the 2026 Texas Renewal Wave is entirely within your control. Homeowners should begin their refinancing preparations at least 12 to 18 months before their loan terms reset. This window allows ample time to improve credit scores, pay down minor debts, and monitor interest rate trends for the optimal lock-in period.

By consulting with a trusted Urbandale, IA mortgage expert, you gain access to customized home loan reports and FICO score insights without the pressure of a hard credit inquiry. The Tyler Osby Team provides weekly updates throughout the application process, ensuring you are never left in the dark about your financial future.

Legal Licensing Information: Fairway Independent Mortgage Corporation, NMLS #2289. Tyler Osby, NMLS #8668, State of Iowa License #19545.

Q1: What is the 2026 Texas Renewal Wave?

It refers to a significant number of adjustable-rate mortgages and interest-only loans that are scheduled to reset or renew in 2026, potentially causing higher monthly payments for homeowners.

Q2: How does a blended rate work in refinancing?

A blended rate calculates the combined average interest rate of multiple loans, such as a primary mortgage and a HELOC. This helps homeowners compare their current total interest costs against a new, single refinance rate.

Q3: What is a breakeven analysis for a mortgage?

A breakeven analysis determines how many months it will take for the monthly savings generated by a lower interest rate to completely offset the closing costs associated with refinancing.

Q4: Can an Urbandale, IA mortgage broker help with complex refinancing scenarios?

Yes, experienced mortgage professionals like The Tyler Osby Team at Fairway Independent Mortgage are equipped to assist clients with advanced scenario modeling and refinancing strategies to protect cash flow.

Q5: When is the optimal time to prepare for a 2026 mortgage reset?

Homeowners should start assessing their options and improving their credit profiles 12 to 18 months before their loan is set to adjust to secure the best possible refinancing terms.