What Mortgage Rates Can Iowa Homebuyers Expect in 2026?

What Mortgage Rates Can Iowa Homebuyers Expect in 2026?

If you are looking to buy a home in Urbandale, Des Moines, or anywhere across Central Iowa, the biggest question on your mind is likely about affordability. After the volatility of the last few years, 2026 is shaping up to be a pivotal year for the housing market. Whether you are a first-time homebuyer or looking to upgrade to your forever home, understanding the mortgage rate landscape is essential to making a smart financial decision.

As we settle into the new year, the “new normal” for interest rates is becoming clearer. While we aren’t seeing the rock-bottom rates of the pandemic era, we are seeing more stability than in previous years. In this comprehensive guide, we will break down what early 2026 rates look like (hovering around 6.4%), expert forecasts for the remainder of the year, and exactly what that means for your monthly mortgage payment on a typical Iowa home.

At The Tyler Osby Team, our goal is simple: to get you into your new home on time, under budget, and with no surprises. Let’s dive into the numbers.

The Early 2026 Landscape: Breaking Down the 6.4% Rate

As we kick off 2026, the average 30-year fixed mortgage rate is trending near 6.4%. For many Iowa homebuyers, this figure represents a stabilization. To understand where we are, it helps to look at the factors driving these numbers.

What is Influencing Rates Right Now?

Mortgage rates are not arbitrary; they are tied closely to the 10-Year Treasury Yield and the broader economic outlook. Several key factors are keeping rates in the mid-6% range early this year:

- Inflation Control: The Federal Reserve has spent the last few years battling inflation. As inflation data stabilizes, lenders feel more confident, reducing the volatility in mortgage pricing.

- Economic Resilience: The labor market in the Midwest, particularly in Des Moines and Urbandale, remains robust. A strong economy generally prevents rates from plummeting, as demand for capital remains high.

- Housing Inventory: In Central Iowa, inventory is slowly recovering, but demand still outpaces supply in popular price brackets.

While 6.4% is higher than the historic lows of 2020-2021, it is historically average. The key for 2026 buyers is to stop waiting for a crash that isn’t coming and start strategizing around the current reality. Start your journey here to see how today’s rates apply to your specific financial situation.

Expert Forecasts: What Does the Rest of 2026 Hold?

Should you lock in a rate now, or wait for a potential drop later in the year? This is the most common question we hear at our Urbandale office. While no one has a crystal ball, financial experts and housing economists have provided consensus forecasts for the remainder of 2026.

Q1 and Q2: Stability is Key

Most analysts predict that rates will remain relatively flat through the spring buying season. We expect rates to fluctuate between 6.2% and 6.6%. This stability is actually good news for buyers; it allows you to budget accurately without fear of a sudden 1% spike overnight.

Q3 and Q4: A Potential Softening?

There is cautious optimism that by the second half of 2026, we may see a slight cooling in rates, potentially dipping closer to 6.0% or slightly below if inflation metrics continue to improve. However, waiting comes with a risk: if rates drop, buyer competition usually heats up.

The “Marry the House, Date the Rate” Philosophy:

Many real estate experts continue to advise that if you find the right home in 2026, you should secure it. If rates drop significantly in 2027 or 2028, refinancing is always an option. However, if home prices in Urbandale continue to rise, waiting for a lower rate might cost you more in the purchase price than you save in interest.

The Real Numbers: Impact on Monthly Payments in Iowa

Percentages are abstract, but monthly payments are reality. Let’s look at how a 6.4% interest rate translates to your bank account based on median home prices in the Des Moines metro area.

For this example, we will use a hypothetical median home price of $325,000—a common price point for a decent single-family home in Urbandale or West Des Moines in 2026.

Scenario: Buying a $325,000 Home

We have broken down the costs based on different down payment amounts. Note: These figures are estimates for Principal and Interest (P&I) only. Taxes and insurance vary by location.

| Down Payment % | Down Payment $ | Loan Amount | Interest Rate | Est. Monthly P&I |

|---|---|---|---|---|

| 3% (First-Time Buyer) | $9,750 | $315,250 | 6.4% | $1,972 |

| 5% (Conventional) | $16,250 | $308,750 | 6.4% | $1,931 |

| 20% (Ideal Scenario) | $65,000 | $260,000 | 6.4% | $1,626 |

As you can see, a small difference in down payment can impact your monthly obligation, but the rate remains the primary driver. If rates were to drop to 6.0%, the payment on that 5% down loan would drop to roughly $1,851—a savings of about $80 a month.

Is waiting for a potential $80 savings worth risking a $15,000 increase in home prices due to appreciation? This is the math Tyler and the team help you calculate before you even make an offer.

How The Tyler Osby Team Secures Competitive Options

In a market where rates are hovering in the mid-6s, who you work with matters more than ever. You aren’t just looking for a loan; you are looking for a strategy. Here is how The Tyler Osby Team at Fairway Independent Mortgage differs from a big-box online lender.

1. Local Knowledge & Relationships

We are based right here in Urbandale. We know the local taxes, the HOA fees in specific developments, and the real estate agents. When we issue a pre-approval letter, listing agents in Central Iowa know it is solid. In a competitive 2026 market, that reputation can get your offer accepted over someone with a generic online pre-qualification.

2. “On Time. Under Budget. No Surprises.”

This isn’t just a slogan; it is our operational promise.

- On Time: We hit our closing dates. We know that delays can cost you money and cause immense stress.

- Under Budget: We look for every opportunity to save you money on closing costs and structure your loan to fit your monthly budget goals.

- No Surprises: We believe in over-communication. You will receive our famous “Friday Updates” so you never go into a weekend wondering where your loan stands.

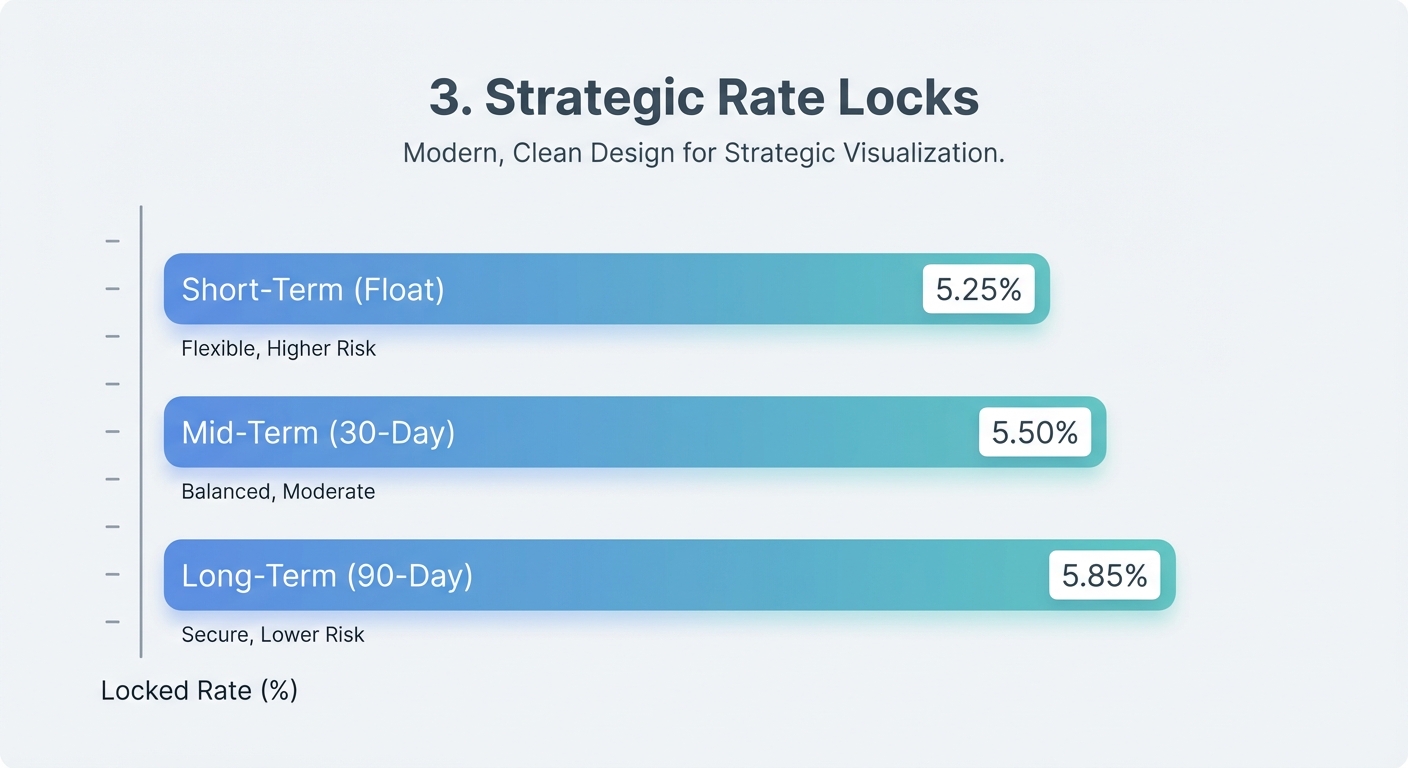

3. Strategic Rate Locks

Actionable Strategies for Iowa Homebuyers in 2026

If you are planning to buy this year, preparation is your best tool for securing a favorable rate.

Boost Your Credit Score

Explore Different Loan Programs

Don’t assume a 30-year fixed Conventional loan is your only option.

- FHA Loans: Often offer lower rates for those with lower credit scores.

- VA Loans: If you are a veteran, this is often the best loan product available, offering 0% down and highly competitive rates.

- ARM (Adjustable Rate Mortgage): In a high-rate environment, a 5/1 or 7/1 ARM can offer a lower introductory rate, giving you time to refinance before the rate adjusts.

Get Fully Pre-Approved, Not Just Pre-Qualified

A pre-qualification is just a guess. A full pre-approval from The Tyler Osby Team involves us verifying your income and assets upfront. This turns you into a “cash-equivalent” buyer in the eyes of sellers. Read more about why this is critical here.

Buying vs. Renting in Urbandale: The 2026 Outlook

With rates at 6.4%, some potential buyers consider continuing to rent. However, rental rates in Des Moines and Urbandale have also seen steady increases. When you buy, you lock in your principal and interest payment for 30 years. When you rent, you are subject to annual increases.

Furthermore, buying builds equity. Even with a modest appreciation rate of 3-4%, a homeowner in Urbandale builds significant wealth over 5 years compared to a renter. We can generate a custom Rent vs. Own analysis for you to see the exact break-even point.

Frequently Asked Questions (FAQs)

1. Will mortgage rates go back down to 3% in 2026?

It is highly unlikely. The rates seen in 2020 and 2021 were a result of a global pandemic and emergency economic measures. Most experts agree that the 5% to 6% range is a more historical norm for a healthy economy.

2. How much do I need for a down payment in Iowa?

Many buyers believe they need 20% down, but that is a myth. Qualified buyers can purchase a home with as little as 3% down (Conventional) or 3.5% down (FHA). Veterans often qualify for 0% down. We can help you find the program that fits your savings.

3. Can I refinance later if rates drop in 2027?

Absolutely. This is a common strategy. If you buy now at ~6.4% and rates drop to 5.4% next year, you can refinance to lower your monthly payment. We monitor rates for all our past clients and will notify you if a refinance makes financial sense.

4. What are closing costs roughly in the Des Moines area?

Closing costs generally range between 2% and 3% of the purchase price. This includes appraisal fees, title insurance, origination fees, and pre-paids for taxes and insurance. We provide a detailed “Total Cost Analysis” so you know exactly what to expect.

5. How long does the mortgage process take with Tyler Osby’s team?

On average, we can close a loan in 30 days or less. However, we have the ability to move faster if a specific closing date requires it. Our “On Time” guarantee means we work backward from your contract date to ensure smooth sailing.

Ready to navigate the 2026 market?

The 2026 housing market in Iowa offers great opportunities for those who are prepared. While rates have shifted, the value of owning a home and building equity remains unchanged. Don’t let headlines paralyze your plans.

Whether you are looking in Urbandale, Waukee, Ankeny, or Des Moines, Tyler Osby and his team are ready to guide you with transparency and expertise. Let’s build a plan that fits your budget.

Click Here to Get Started with a Free Consultation

The Tyler Osby Team at Fairway Independent Mortgage Corporation.

2400 86th Street, Suite 29, Urbandale, IA 50322

Phone: (515) 991-7102 | Email: tyler@tylerosbyteam.com

Copyright© 2026 Fairway Independent Mortgage Corporation. NMLS#2289. 4750 S. Biltmore Lane, Madison, WI 53718, 1-866-912-4800. All rights reserved. Tyler Osby, Branch Manager, NMLS #8668. This is not an offer to enter into an agreement. Not all customers will qualify. Information, rates, and programs are subject to change without prior notice. All products are subject to credit and property approval. Other restrictions and limitations may apply. Equal Housing Opportunity.