The Ultimate Guide to Doctor Mortgage Loans in Urbandale, IA

What Are Physician and Professional-Program Mortgages?

Medical professionals and legal experts dedicate years to education and training. When it is time to buy a home in Urbandale, IA, traditional financing might not always align with the unique financial situations of recent graduates or practicing professionals. Enter the doctor mortgage loan. Also known as physician professional-program mortgages, these specialized loan options are designed to help high-income earners secure a home even if they have substantial student debt or have not built a massive down payment.

Whether you are a newly matched resident or a practicing attorney, navigating these Doctor Loans can be complex. The Tyler Osby Team at Fairway Independent Mortgage is here to help you understand your options. We are experts at providing second opinions on physician and professional mortgage programs, ensuring you get the best terms possible. While some buyers might explore a conventional fixed-rate mortgage, professional programs often offer superior benefits tailored just for you.

Key Benefits for Doctors, Dentists, and Lawyers

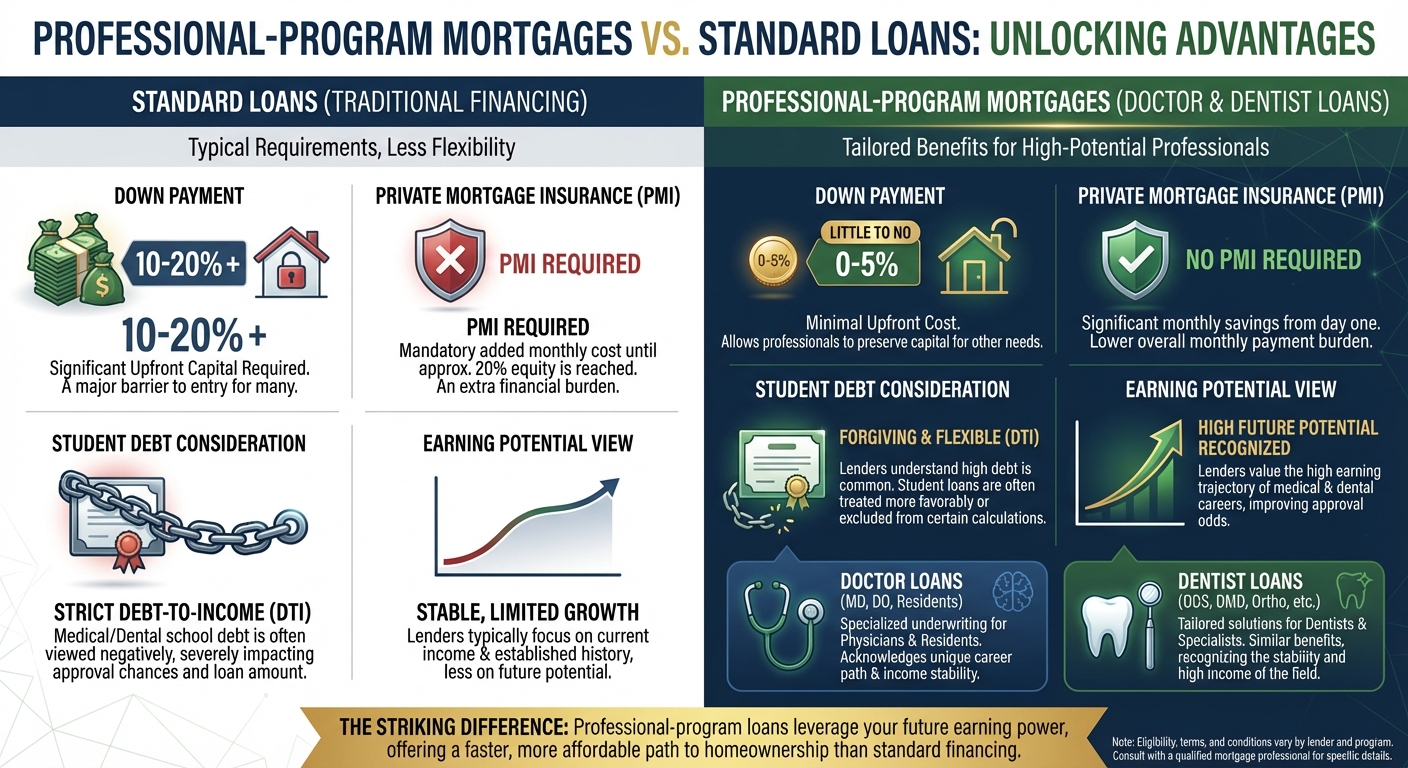

Professional-program mortgages offer incredible advantages that standard loans simply cannot match. If you are comparing a standard loan to a doctor mortgage loan, the differences are striking.

- Doctor Loans: Medical doctors and residents can often secure financing with little to no down payment and no Private Mortgage Insurance (PMI). Lenders understand that your earning potential is high, so they are more forgiving of medical school debt.

- Dentist Loans: Just like medical doctors, dentists and orthodontists face high educational costs. Dentist loans provide the same flexible debt-to-income calculations, allowing you to purchase your dream home in Urbandale without waiting years to save.

- Lawyer Loans: Attorneys also benefit from professional mortgage programs. If you are a practicing lawyer or a newly minted associate, these loans help you bypass strict conventional guidelines.

These programs are incredibly useful if you are looking at higher-priced real estate and might otherwise need a jumbo mortgage. By excluding deferred student loans from your debt-to-income ratio, a professional loan opens doors that might otherwise remain closed.

| Feature | Standard Conventional Loan | Doctor Mortgage Loan |

|---|---|---|

| Down Payment | Typically 3% to 20% | 0% to 5% in many cases |

| Private Mortgage Insurance (PMI) | Required if down payment is under 20% | Usually waived entirely |

| Student Loan Debt Calculation | Strictly included in debt-to-income ratio | Often excluded or heavily discounted |

| Employment Requirements | Requires 2 years of steady employment history | Can often close before starting a new job with a signed contract |

Why Choose The Tyler Osby Team for Your Professional Loan?

Securing a doctor mortgage loan requires working with a lender who truly understands the nuances of professional financial profiles. As the most recommended mortgage lender in Iowa, Tyler Osby and his team have helped countless medical and legal professionals in Urbandale, IA, achieve their homeownership goals. With over 1,300 five-star Google reviews, our reputation speaks for itself.

We specialize in providing expert second opinions on physician and professional mortgage programs. If you have already received a quote, let us review it to ensure you are getting the optimal deal. Reach out to us at tyler@tylerosbyteam.com or call 15159917102 to get started.

Legal Licensing Information: Fairway Independent Mortgage Corporation, NMLS #2289. Tyler Osby, NMLS #8668, State of Iowa License #19545.

Q1: What is a doctor mortgage loan?

A doctor mortgage loan is a specialized home financing option designed for medical professionals. It typically offers zero or low down payment requirements and does not require private mortgage insurance, even with high student loan debt.

Q2: Do dentist and lawyer loans work the same way?

Yes, dentist and lawyer loans operate under similar professional-program mortgage guidelines. They provide flexible debt-to-income calculations and favorable terms tailored to high-earning professionals with significant educational debt.

Q3: Can I get a professional mortgage before I start my new job in Urbandale, IA?

Absolutely. Many physician professional-program mortgages allow you to close on a home up to 90 days before you begin your new employment, provided you have a signed contract.

Q4: How does a doctor loan compare to a jumbo mortgage?

While a jumbo mortgage is used for high-value properties and often requires a strict down payment and pristine credit, a doctor loan can also cover high loan amounts but offers more leniency regarding student debt and down payments.

Q5: How can I get a second opinion on my current mortgage offer?

The Tyler Osby Team is happy to provide a no-obligation consultation. You can reach out to us at tyler@tylerosbyteam.com or call 15159917102 to discuss your current offer and see if we can find a better professional program for you. Apply Online with The Tyler Osby Team Today