First-Time Homebuyers in Houston 2026: Creative Paths to Ownership When Prices Feel High

Navigating the 2026 Houston Real Estate Market

The Houston real estate market continues to evolve as we approach 2026. For many first-time buyers, property prices might feel intimidating. However, creative financing paths and expert guidance can make your dream of homeownership a reality.

At The Tyler Osby Team, located in Urbandale, IA, we frequently assist clients who are exploring relocations or seeking top-tier mortgage education. Whether you are moving from Iowa to Texas or simply want to understand the best financing strategies, knowing your options is the first step.

Houston offers a diverse range of neighborhoods and property types. To succeed in this competitive landscape, buyers must leverage specific mortgage programs designed to lower barriers to entry. In this guide, we will explore tactical approaches using various loan types to help you secure a home in Houston.

Tactical Mortgage Solutions: FHA, VA, and Conventional Loans

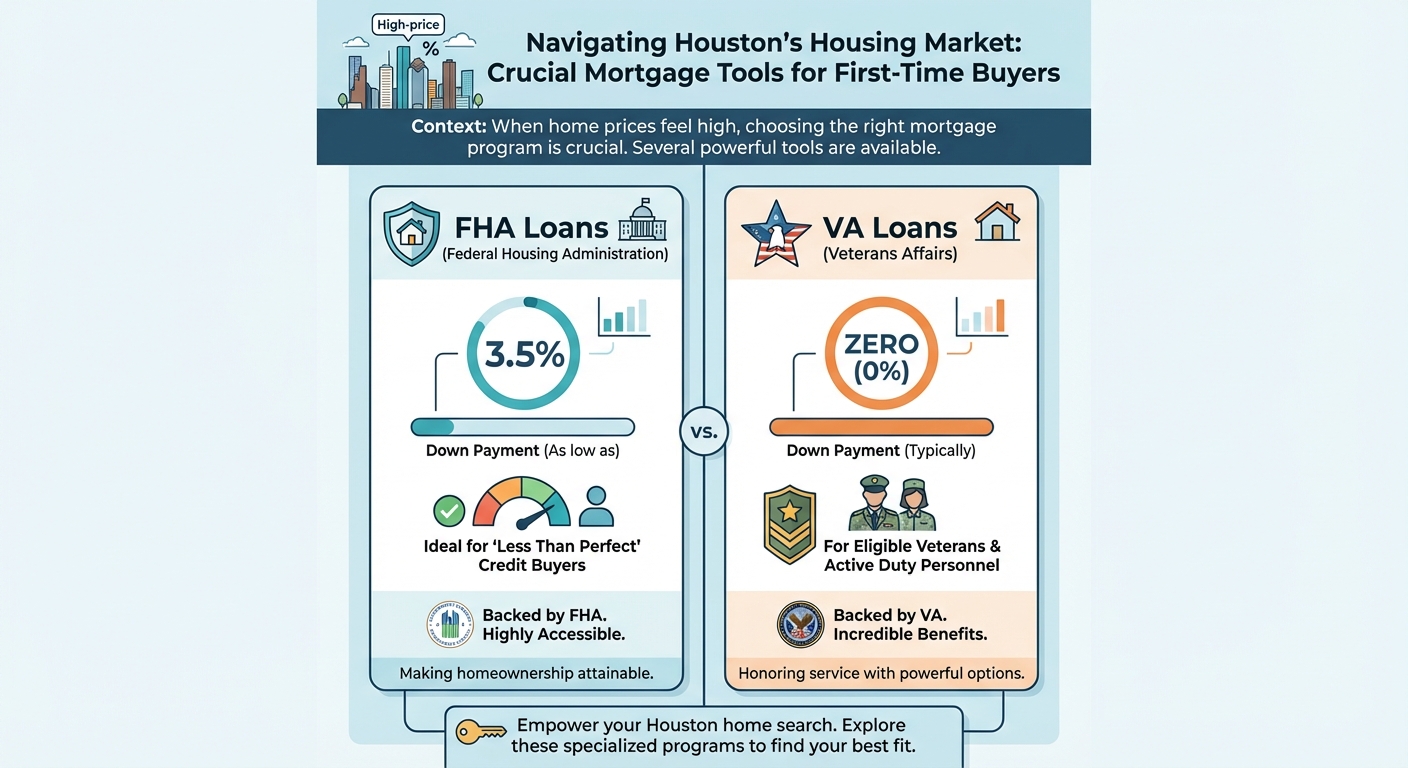

When home prices feel high, choosing the right mortgage program is crucial. First-time homebuyers in Houston have several powerful tools at their disposal.

- FHA Loans: Backed by the Federal Housing Administration, these loans are perfect for buyers with less than perfect credit. They require a down payment as low as 3.5 percent, making them highly accessible.

- VA Loans: For eligible veterans and active duty military personnel, VA loans offer incredible benefits. They typically require zero down payment and do not require private mortgage insurance (PMI).

- Conventional Loans: If you have a strong credit score, a conventional loan might be your best route. First-time buyers can often secure a conventional mortgage with just 3 percent down.

- Texas Specific Programs: The Texas State Affordable Housing Corporation (TSAHC) and the Texas Department of Housing and Community Affairs (TDHCA) provide down payment assistance grants and favorable interest rates for eligible buyers.

Partnering with an experienced mortgage broker ensures you find the exact program that fits your financial profile. The Tyler Osby Team is dedicated to providing weekly updates and transparent communication throughout your entire application process.

| Loan Program | Minimum Down Payment | Minimum Credit Score (Typical) | Best For |

|---|---|---|---|

| FHA Loan | 3.5% | 580 | Buyers needing flexible credit requirements |

| VA Loan | 0% | 620 (Varies by lender) | Veterans and active duty military |

| Conventional | 3.0% | 620 | Buyers with strong credit histories |

| Texas TSAHC | Varies (Grants available) | 620 | First-time buyers needing down payment help |

Planning Your 2026 Home Purchase with Confidence

Preparation is the key to unlocking creative paths to ownership. Before you start touring homes in Houston, you need a solid financial foundation. We recommend starting with a no obligation consultation to review your custom home loan report and FICO score.

Here are a few actionable steps to prepare for your 2026 home purchase:

- Review Your Credit: Ensure your credit report is accurate. A higher score unlocks better interest rates.

- Save for Closing Costs: Even with zero down programs, closing costs are a factor. Ask your lender about seller concessions or lender credits.

- Get Pre-Qualified: A pre-qualification letter shows sellers you are a serious buyer. You can take about 10 minutes to complete our online application to get started.

Our clients consistently praise our high character, integrity, and seamless process. As the most recommended mortgage lender in Iowa, we bring that same level of care to every conversation, no matter where your homebuying journey takes you. Contact Tyler Osby at tyler@tylerosbyteam.com or call 1-515-991-7102 today.

Legal Licensing Information: Fairway Independent Mortgage Corporation, NMLS #2289. Tyler Osby, NMLS #8668, State of Iowa License #19545.

Q1: What is the minimum down payment for a house in Houston in 2026?

First-time homebuyers can often purchase a home with as little as 0 to 3.5 percent down, depending on whether they qualify for VA, Conventional, or FHA loans.

Q2: Are there specific mortgage programs for Texas residents?

Yes, programs through the TSAHC and TDHCA offer down payment assistance and competitive interest rates specifically for Texas homebuyers.

Q3: Can an Urbandale, IA mortgage broker help me if I am moving to Texas?

Absolutely. The Tyler Osby Team can provide expert guidance, evaluate your financial profile, and connect you with the right resources for your out-of-state relocation.

Q4: How do FHA loans help when home prices feel high?

FHA loans allow for lower credit scores and smaller down payments, which reduces the initial cash required to purchase a home in a competitive market.

Q5: How long does the pre-qualification process take?

You can complete the initial online application in about 10 minutes. Afterward, we schedule a one-on-one consultation to discuss your specific loan options.