The Contrarian Mortgage Guide 2026: Myths That Keep Borrowers Overpaying (And the Real Fixes)

Shattering the Single-Lender Loyalty Illusion

When it comes to securing a home loan in 2026, old habits will cost you dearly. Whether you are analyzing the booming real estate market or searching for a home right here in Urbandale, IA, borrowers are falling into the exact same costly traps. The most expensive trap of all? Blind loyalty to a single bank.

Many homebuyers believe that sticking with their childhood bank will unlock hidden discounts or preferential treatment. In reality, retail banks often have higher overhead and limited loan products. Working with an experienced mortgage professional like the Tyler Osby Team provides access to a wider variety of loan options and competitive rates.

- The Myth: Your primary bank will give you the best rate because of your long-standing relationship.

- The Reality: Banks offer only their own proprietary products, which may not fit your unique financial situation.

- The Fix: Shop around or use a dedicated mortgage broker who can compare multiple options for you without causing unnecessary stress.

By breaking free from single-lender loyalty, you position yourself to save thousands over the life of your loan. This contrarian approach is the first step to truly optimizing your mortgage strategy.

The Credit Score Obsession and Timing Fallacies

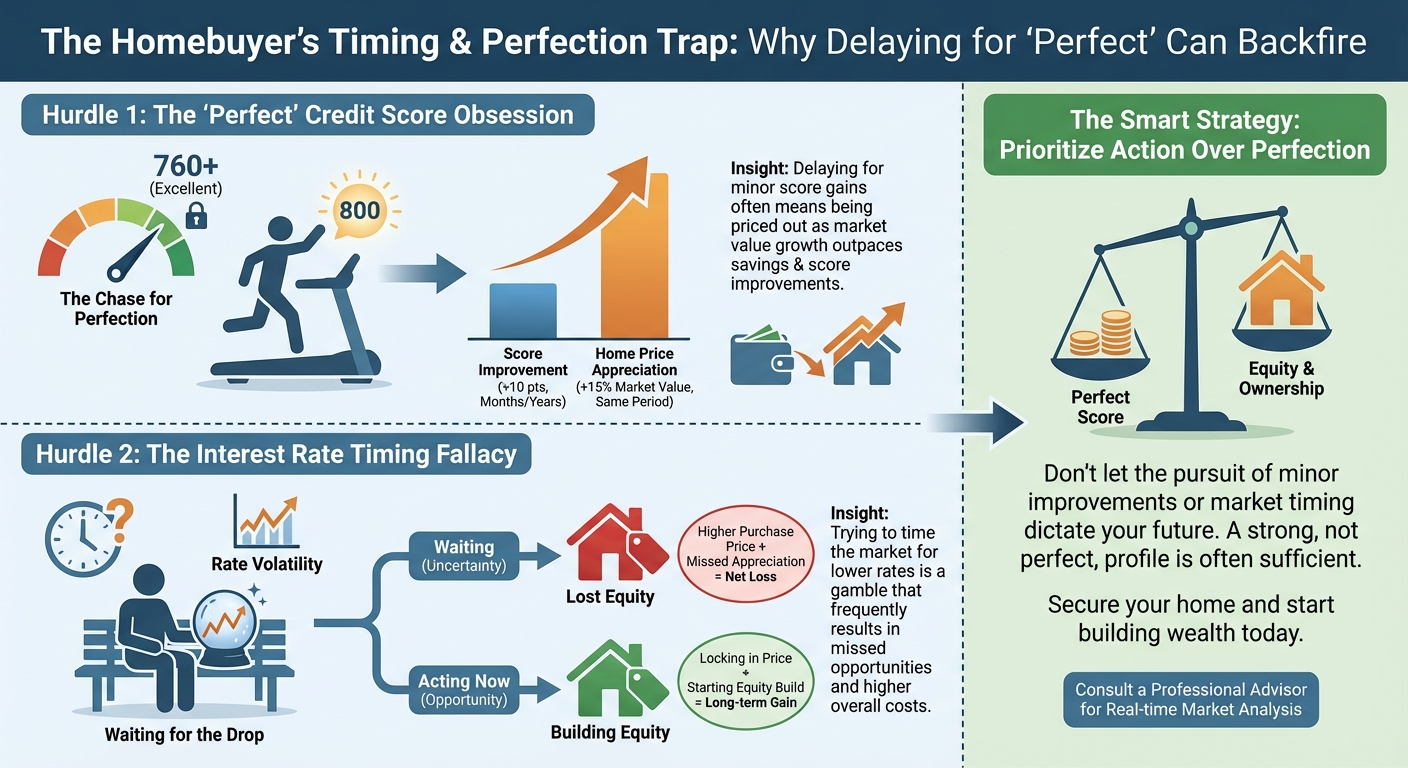

Another major hurdle for modern buyers is the relentless obsession with achieving a perfect credit score before applying for a mortgage. While a strong credit profile is important, delaying your purchase to squeeze out a few extra points can actually backfire. In highly competitive markets, home prices can appreciate faster than your savings or credit score improvements can keep up with.

Alongside the credit score myth is the ultimate timing fallacy: waiting for interest rates to drop. Let us look at why trying to time the market is a flawed strategy:

- Lost Equity: Every month you wait is a month you are not building equity in a property.

- Increased Competition: When rates drop, buyer demand surges. This drives up home prices and often leads to stressful bidding wars.

- Refinancing Opportunities: You can always refinance your rate later, but you cannot renegotiate the purchase price of your home once it is sold to someone else.

Whether you are moving across the country or settling down in Urbandale as a first-time buyer, focusing on your monthly budget rather than a magical interest rate number is the smartest contrarian move you can make in 2026.

| Mortgage Myth | The Costly Reality | The Contrarian Fix |

|---|---|---|

| Loyalty pays off with big banks | Limited loan products and potentially higher rates | Work with a mortgage expert to shop multiple lenders |

| Wait for an 800 credit score | Home prices rise faster than your score improves | Buy when you are financially ready, not artificially perfect |

| Time the market for lower rates | Lower rates trigger bidding wars and higher home prices | Marry the house, date the rate (plan to refinance later) |

Real Fixes for the Modern Homebuyer

To stop overpaying, you need a strategy built on facts, not outdated advice. The real fix is partnering with a transparent, communicative mortgage team that puts your needs first. With over 1,300 five-star reviews, the Tyler Osby Team is dedicated to guiding buyers through the noise. We provide weekly updates, custom home loan reports, and a no-obligation consultation to ensure you are making the best financial decision.

Remember, the goal is to secure a home that fits your life and your budget. Do not let myths dictate your future. Start by getting a clear picture of your options with a pre-qualification process designed to protect your peace of mind.

Legal Licensing Information: Fairway Independent Mortgage Corporation, NMLS #2289 Tyler Osby, NMLS #8668, State of Iowa License #19545.

Q1: Do I need a perfect credit score to buy a house in 2026?

No. While a good score helps secure better rates, waiting for a perfect score can cost you in lost equity and rising home prices. There are many loan programs available for various credit profiles.

Q2: Is it better to wait for interest rates to drop before buying?

Trying to time the market is a common fallacy. When rates drop, buyer competition increases, often driving home prices up. It is generally better to buy when you are financially ready and refinance later if rates improve.

Q3: Why should I use a mortgage professional instead of my primary bank?

A dedicated mortgage team has access to multiple loan products, allowing them to find the best terms for your specific situation. Big retail banks typically only offer their own limited in-house products.

Q4: Can the Tyler Osby Team help me if I am relocating to Iowa?

Absolutely. Whether you are moving locally to Urbandale, IA, or relocating from out of state, the Tyler Osby Team provides seamless digital communication and weekly updates to keep your loan on track from anywhere.

Q5: Will applying for a mortgage pre-qualification hurt my credit?

Getting started with the Tyler Osby Team involves a process with no hard credit inquiry initially, allowing you to review your options and FICO score without negatively impacting your credit profile.