Your Guide to a Conventional Fixed-Rate Mortgage in Urbandale, IA

What is a Conventional Mortgage?

When you are ready to buy a home in Urbandale, IA, choosing the right financing is a critical step. A conventional mortgage is one of the most popular loan options available for homebuyers today. Unlike government-backed loans such as an FHA purchase loan, a conventional fixed-rate mortgage is not insured by the federal government. Instead, it is backed by private lenders and often purchased by Fannie Mae or Freddie Mac.

Opting for a 30-year fixed-rate mortgage provides the stability of knowing exactly what your principal and interest payments will be for the life of the loan. At The Tyler Osby Team, we understand that navigating your mortgage options can feel overwhelming. That is why we are experts at providing second opinions on conventional mortgages. If you already have a quote from another lender, let our local Urbandale experts review it to ensure you are getting the best possible terms for your financial future.

Conforming vs. Non-Conforming Conventional Loans

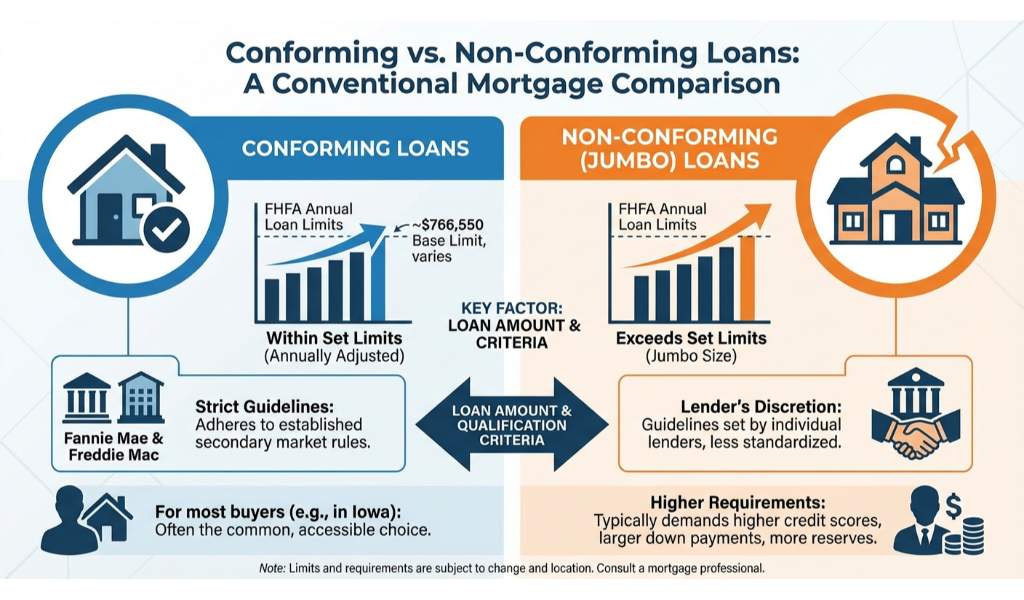

Understanding the difference between conforming and non-conforming loans is essential when exploring a conventional mortgage. These two categories dictate the size of the loan you can secure and the specific requirements you must meet to qualify.

- Conforming Loans: These loans fall within the maximum loan limits set annually by the Federal Housing Finance Agency (FHFA). They conform to the strict guidelines established by Fannie Mae and Freddie Mac. For most buyers in Iowa, a conforming loan is the standard path to homeownership.

- Non-Conforming Loans: If you need to borrow an amount that exceeds the FHFA limits, you will need a non-conforming loan, commonly referred to as a jumbo mortgage. Because these loans cannot be purchased by Fannie Mae or Freddie Mac, they carry slightly different credit, reserve, and down payment requirements.

Whether you are looking at a standard conforming loan for a starter home or a larger non-conforming loan for your dream property, our Urbandale team is here to guide you through the application process with complete transparency.

| Feature | Conforming Conventional Mortgage | Non-Conforming (Jumbo) Mortgage |

|---|---|---|

| Loan Limits | Subject to annual FHFA limits | Exceeds FHFA limits |

| Credit Score Requirement | Typically 620 or higher | Usually requires a stricter credit profile (often 700+) |

| Down Payment | As low as 3% for first-time buyers | Typically 10% to 20% or more |

| Government Backing | None (Backed by Fannie Mae / Freddie Mac) | None (Held by private investors) |

Why Choose The Tyler Osby Team for Your Home Loan?

Finding the right lender for your conventional mortgage is just as important as finding the perfect house. The Tyler Osby Team at Fairway Independent Mortgage is proud to be the most recommended mortgage lender in Iowa. With over 1,300 five-star reviews on Google, our reputation in Urbandale and beyond speaks for itself. We believe in providing a stress-free experience, complete with weekly updates and a simple 10-minute online application.

We highly encourage borrowers to seek a second opinion on their loan estimates. Our team will gladly review your current pre-approval to see if a conventional fixed-rate mortgage could save you money. Legal Licensing Information: Fairway Independent Mortgage Corporation, NMLS #2289. Tyler Osby, NMLS #8668, State of Iowa License #19545.

Q1: What is the minimum down payment for a conventional mortgage?

For a conventional mortgage, first-time homebuyers can often secure a loan with as little as 3% down, while repeat buyers typically need at least 5%.

Q2: Do I have to pay mortgage insurance on a conventional fixed-rate mortgage?

Private Mortgage Insurance (PMI) is usually required if your down payment is less than 20%. However, unlike some government loans, PMI on a conventional loan can be canceled once you reach 20% equity in your home.

Q3: Can I get a second opinion on my conventional mortgage quote?

Absolutely! The Tyler Osby Team specializes in providing expert second opinions on conventional mortgages to ensure you receive the most favorable terms in Urbandale, IA.

Q4: How does a conventional loan differ from an FHA loan?

An FHA loan is backed by the government and often has more flexible credit requirements, whereas a conventional mortgage is not government-insured and typically requires a higher credit score but offers more flexible property standards.

Q5: What credit score is needed for a conventional mortgage?

Most lenders require a minimum credit score of 620 to qualify for a conforming conventional mortgage, though higher scores generally unlock better interest rates and lower PMI costs.Apply Online with The Tyler Osby Team Today