What is an Adjustable-Rate Mortgage (ARM)?

If you are exploring home financing options in Urbandale, IA, you might have heard about the adjustable rate mortgage. Often referred to simply as an ARM, this loan type offers an initial period with a fixed interest rate, followed by a period where the rate adjusts based on current market conditions. For many Iowa homebuyers, an ARM can be a highly strategic choice to secure lower initial monthly payments compared to a traditional 30-year fixed rate mortgage or a 15-year fixed rate mortgage.

At The Tyler Osby Team at Fairway Independent Mortgage, we are experts at providing second opinions on adjustable-rate mortgages. Whether you are considering a 3/1 ARM for a short-term living situation or a 10/1 ARM for longer stability, understanding the mechanics of these loans is crucial to making an informed financial decision. A well-structured ARM could save you thousands of dollars in interest during the initial fixed period.

Understanding ARM Structures: 5/1, 5/6, 7/6, and 10/1 ARMs

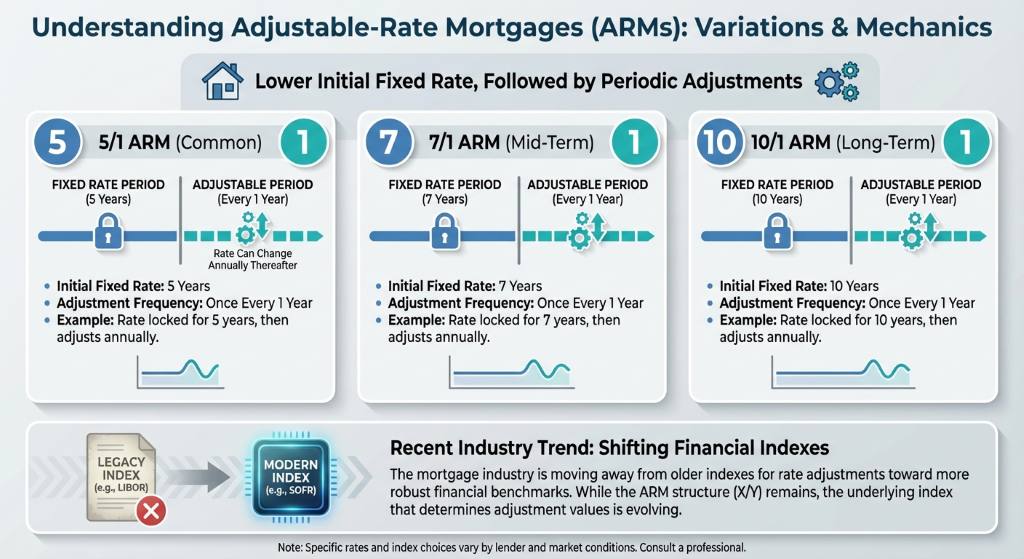

Adjustable-rate mortgages come in several variations, with the most common historically being the 5/1 ARM, 7/1 ARM, and 10/1 ARM. The first number represents the number of years the interest rate remains fixed. The second number indicates how often the rate can adjust after the initial period ends. For example, a 5/1 ARM keeps your rate locked for five years and then adjusts once every year thereafter.

Recently, the mortgage industry has shifted toward loans tied to different financial indexes, leading to the rise of the 5/6 ARM and 7/6 ARM. In a 5/6 ARM, your rate is fixed for five years, but it adjusts every six months rather than annually. These structures are also widely available if you are looking at a jumbo mortgage for a luxury property in Urbandale. If you currently have an ARM and your fixed period is ending soon, you might also consider a rate and term refinance to switch to a predictable fixed-rate loan.

| ARM Type | Initial Fixed Period | Adjustment Frequency |

|---|---|---|

| 3/1 ARM | 3 Years | Annually |

| 5/1 ARM | 5 Years | Annually |

| 5/6 ARM | 5 Years | Every 6 Months |

| 7/1 ARM | 7 Years | Annually |

| 7/6 ARM | 7 Years | Every 6 Months |

| 10/1 ARM | 10 Years | Annually |

Are Caps and Floors Important for Your Home Loan?

One of the most critical components of any adjustable rate mortgage is the system of caps and floors. These built-in safeguards dictate exactly how much your interest rate can change, protecting you from extreme market fluctuations.

- Initial Cap: Limits how much the rate can increase the very first time it adjusts.

- Periodic Cap: Restricts the amount the rate can change during subsequent adjustment periods.

- Lifetime Cap: The absolute maximum interest rate you can be charged over the life of the loan.

- Floors: The minimum interest rate your loan can drop to, regardless of how low market indexes fall.

Understanding these limits is essential for your peace of mind. As your trusted local mortgage professionals in Urbandale, Tyler Osby and his team are here to help you review these details. We highly recommend getting a second opinion if you are unsure about the caps and floors outlined in your current loan estimate.

Legal Licensing Information: Fairway Independent Mortgage Corporation, NMLS #2289. Tyler Osby, NMLS #8668, State of Iowa License #19545.

Q1: What is an adjustable rate mortgage?

An adjustable rate mortgage (ARM) is a home loan with an interest rate that remains fixed for a specific initial period, after which the rate adjusts periodically based on current market indexes.

Q2: What is the difference between a 5/1 ARM and a 5/6 ARM?

A 5/1 ARM adjusts annually after the first five years, while a 5/6 ARM adjusts every six months after the initial five-year fixed period ends.

Q3: Are there limits to how high my ARM rate can go?

Yes, adjustable-rate mortgages include lifetime caps and periodic caps to prevent your interest rate from rising beyond a specified maximum percentage.

Q4: Can I refinance my adjustable-rate mortgage before it adjusts?

Absolutely. Many homeowners choose a rate and term refinance to switch to a fixed-rate mortgage before their initial fixed period expires.

Q5: Does The Tyler Osby Team offer second opinions on ARMs?

Yes, we are experts at providing second opinions on adjustable-rate mortgages for homebuyers in Urbandale and throughout Iowa to ensure you get the best possible loan structure.Get Your Free Mortgage Consultation Today