Understanding the Basics of a Conventional Mortgage

When you are ready to buy a home in Urbandale, IA, navigating your loan options can feel overwhelming. A conventional fixed-rate mortgage is often the gold standard for buyers with strong credit and a steady income. Also known simply as a conventional mortgage, this type of loan is not backed by a government agency like the FHA or VA. Instead, it follows guidelines set by Fannie Mae and Freddie Mac.

At The Tyler Osby Team at Fairway Independent Mortgage, we pride ourselves on helping Iowa families secure the right financing. Whether you are buying your first house or looking for a second opinion on conventional mortgages, our team is here to help. A popular choice among buyers is the 30-year fixed-rate mortgage because it offers predictable monthly payments for the life of the loan. If you are comparing this to other options, you might also want to explore an FHA purchase loan to see which fits your financial goals best.

Conforming vs Non-Conforming Loans: What You Need to Know

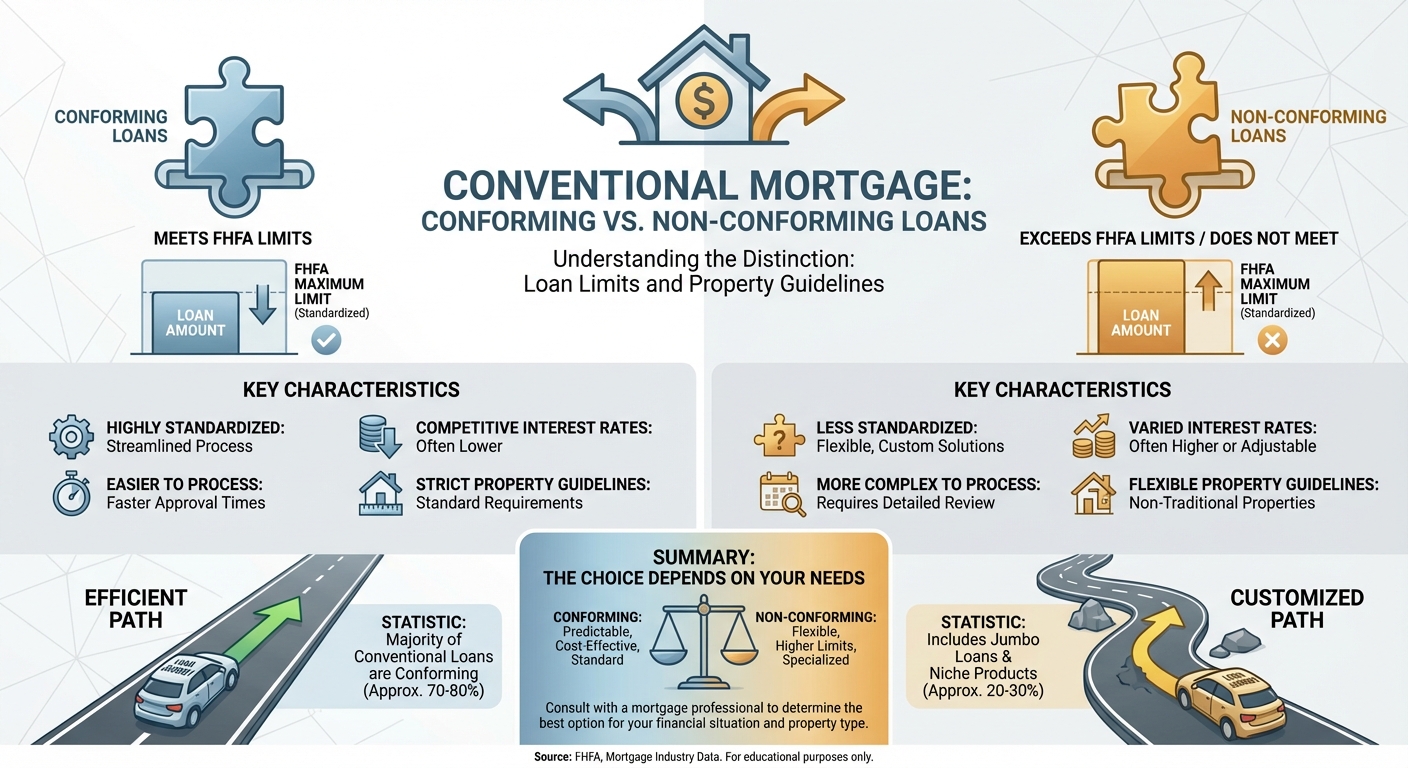

When discussing a conventional mortgage, it is crucial to understand the difference between conforming and non-conforming loans. This distinction primarily comes down to loan limits and property guidelines.

- Conforming Loans: These loans fall within maximum limits set by the Federal Housing Finance Agency (FHFA). They are highly standardized, making them easier to process and often offering highly competitive interest rates.

- Non-Conforming Loans: These loans exceed the FHFA limits or do not meet standard guidelines. A common example is a jumbo mortgage, which is necessary when purchasing luxury properties or homes in highly competitive real estate markets.

Choosing between these two depends heavily on your budget and the home you wish to purchase in the Urbandale area. If you already have a quote from another lender, remember that we are experts at providing second opinions on conventional mortgages. We will carefully review your numbers to ensure you are getting the best possible terms.

| Feature | Conforming Conventional Mortgage | Non-Conforming (Jumbo) Mortgage |

|---|---|---|

| Loan Limits | Adheres to annual FHFA limits | Exceeds FHFA limits |

| Credit Score Requirement | Typically 620 or higher | Usually requires 700 or higher |

| Down Payment | As low as 3% for first-time buyers | Typically 10% to 20% or more |

| Interest Rates | Highly competitive and standardized | Can be slightly higher due to increased risk |

Why Choose The Tyler Osby Team for Your Home Loan?

Securing a conventional fixed-rate mortgage should be a smooth and transparent process. With over 1,300 five-star Google reviews, The Tyler Osby Team is dedicated to clear communication. We provide weekly updates so you always know exactly where your application stands. Our goal is to make homeownership in Iowa as stress-free as possible.

Legal Licensing Information: Fairway Independent Mortgage Corporation, NMLS #2289. Tyler Osby, NMLS #8668, State of Iowa License #19545.

If you are exploring a conventional mortgage and want a team that truly cares about your financial well-being, we invite you to experience our top-tier customer service. We offer no-obligation consultations and custom home loan reports tailored specifically to your needs.

Q1: What is a conventional fixed-rate mortgage?

A conventional fixed-rate mortgage is a home loan not insured by the federal government. It features an interest rate that remains the same for the entire life of the loan, providing predictable monthly payments.

Q2: Can I get a second opinion on my conventional mortgage offer?

Absolutely. We are experts at providing second opinions on conventional mortgages. We can review your current pre-approval to ensure you are receiving the most competitive rates and terms available in Urbandale, IA.

Q3: What is the minimum down payment for a conventional mortgage?

While many people believe you need 20 percent down, first-time homebuyers can often secure a conventional mortgage with as little as 3 percent down.

Q4: How do I know if I need a conforming or non-conforming loan?

It depends on the price of the home you are buying. If your loan amount is below the local FHFA limit, you will use a conforming loan. If it exceeds that limit, you will need a non-conforming loan such as a jumbo mortgage.

Q5: Does The Tyler Osby Team offer loans outside of Urbandale, IA?

Yes! While we are highly active in Urbandale, we are licensed to help homebuyers throughout the entire state of Iowa find the perfect conventional mortgage.