Understanding Down Payment Assistance Options in Urbandale

Buying a home is an exciting milestone, but coming up with the initial funds can feel overwhelming. Fortunately, Down Payment Assistance Programs are designed to bridge the gap between your savings and your dream home. Also known simply as Down Payment Assistance, these initiatives provide financial support to qualified buyers to help cover upfront costs.

Whether you are looking for a first-time homebuyer mortgage or transitioning to a new property in Urbandale, IA, understanding your options is the first step toward affordable homeownership. At The Tyler Osby Team, we specialize in helping Iowa residents navigate these local and national programs to find the perfect fit for their financial goals.

Types of Down Payment Assistance: Grants, Forgivable Loans, and Second Liens

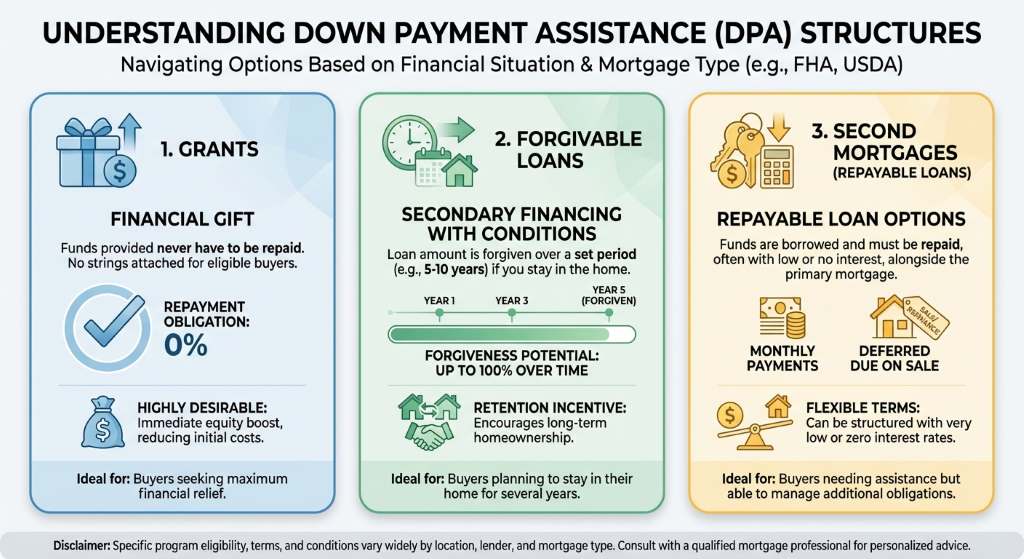

Not all Down Payment Assistance Programs operate the same way. Depending on your financial situation and the type of mortgage you choose, such as an FHA purchase loan or a USDA rural development loan, you might qualify for different structures of assistance. Here is a comprehensive look at the three primary categories:

- Grants: This is essentially a financial gift. Grants provide funds that never have to be repaid, making them highly desirable for eligible buyers.

- Forgivable Loans: These are second mortgages with a zero percent interest rate. If you stay in the home for a specified number of years, the loan is completely forgiven. If you move or refinance early, you may need to repay a prorated amount.

- Second Liens: Sometimes called deferred payment loans, these require you to pay back the assistance amount when you sell the home, refinance, or pay off your primary mortgage. They often carry low or zero interest.

Because the rules and qualifications can be complex, we highly recommend working with a trusted local mortgage broker. In fact, we are experts at providing second opinions on down payment assistance programs to ensure you are truly getting the best deal available.

| Assistance Type | Repayment Required? | Best For |

|---|---|---|

| Grants | No repayment needed | Buyers who meet specific income or location criteria seeking immediate equity. |

| Forgivable Loans | Forgiven over time (usually 3 to 10 years) | Homeowners planning to stay in their new property long-term. |

| Second Liens | Repaid upon sale, refinance, or payoff | Buyers needing extra funds upfront who are comfortable repaying later. |

Why Get a Second Opinion on Down Payment Assistance Programs?

When navigating the mortgage landscape, settling for the first offer you receive can sometimes leave money on the table. Mortgage terms, interest rates, and specific program eligibility vary significantly from lender to lender. We are experts at providing second opinions on down payment assistance programs, ensuring that your customized home loan report actually reflects the most advantageous path for your family.

With over 1,300 five-star reviews on Google, The Tyler Osby Team is dedicated to transparency, high character, and integrity. We will review your current pre-qualification, compare it against available grants and forgivable loans, and give you an honest assessment of your options.

Legal Licensing Information: Fairway Independent Mortgage Corporation, NMLS #2289 Tyler Osby, NMLS #8668, State of Iowa License #19545.

Q1: What are Down Payment Assistance Programs?

Down Payment Assistance Programs are specialized financial initiatives offered by state, local, or federal organizations to help homebuyers cover the upfront costs of purchasing a home. They can come in the form of grants, forgivable loans, or deferred second liens.

Q2: Do I have to be a first-time homebuyer to qualify for Down Payment Assistance?

While many programs are targeted toward first-time homebuyers, there are several options available for repeat buyers. Eligibility often depends on your household income, the location of the property, and the specific program guidelines.

Q3: Are down payment assistance grants completely free money?

Yes, grants are considered a gift and do not need to be repaid. However, they usually come with strict eligibility requirements regarding income limits and purchase price caps.

Q4: How do forgivable loans work?

A forgivable loan acts as a second mortgage, often with a 0% interest rate. A portion of the loan is forgiven each year you live in the home. If you stay for the entire required term, the loan is completely forgiven and you owe nothing.

Q5: Can I combine down payment assistance with other loan types?

Absolutely. Down Payment Assistance can frequently be paired with various primary mortgages, including an FHA purchase loan, a USDA rural development loan, or a conventional mortgage, depending on the program’s specific rules.Get Your Custom Home Loan Report Today