What is an FHA 203k Renovation Loan?

If you are house hunting in Urbandale, IA, you might have noticed that finding the perfect move-in ready home can be a challenge. That is where an FHA 203k loan comes in. Also known as an FHA 203k Renovation loan, this unique mortgage program allows you to finance both the purchase of a house and the cost of its repairs through a single mortgage.

Unlike a standard FHA purchase loan, the 203k program is specifically designed for properties that need some TLC. Whether you are looking to update an outdated kitchen, repair a leaky roof, or completely remodel a historic property, an FHA 203k loan gives you the financial flexibility to turn a fixer-upper into your dream home.

At The Tyler Osby Team at Fairway Independent Mortgage, we are experts at providing second opinions on FHA 203k renovation loans. If you have been told a project is not possible by another lender, let us take a look and find a path forward.

Standard 203(k) vs. Limited 203(k): Which is Right for You?

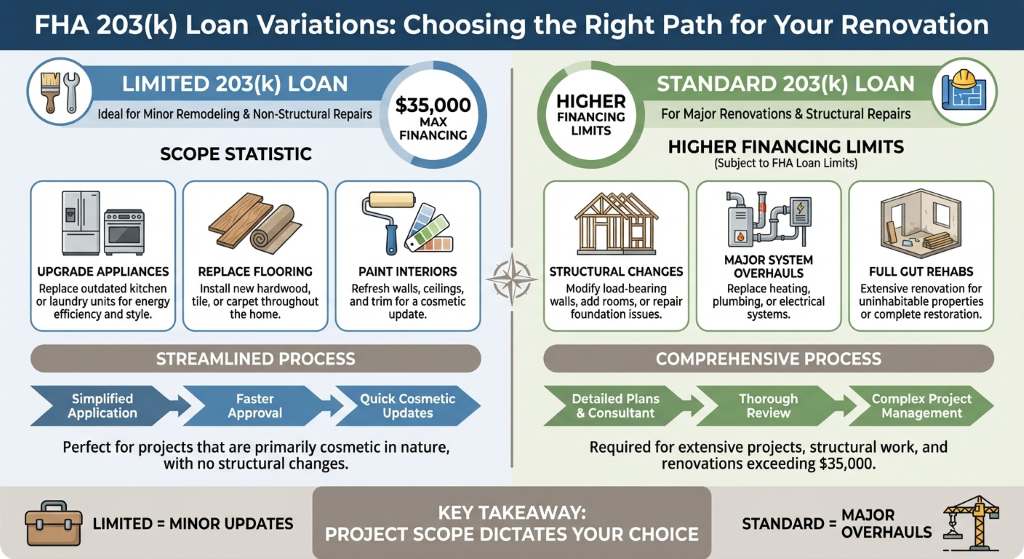

When exploring an FHA 203k loan, it is crucial to understand that there are two distinct variations: the Standard 203(k) and the Limited 203(k). Choosing the right one depends entirely on the scope of your renovation project.

- The Limited 203(k) Loan: This option is ideal for minor remodeling and non-structural repairs. It allows you to finance up to $35,000 into your mortgage to upgrade appliances, replace flooring, or paint the interiors. It is a streamlined process perfect for cosmetic updates.

- The Standard 203(k) Loan: If your future Urbandale home requires major rehabilitation, such as structural alterations, room additions, or foundation work, the Standard 203(k) is the way to go. There is no maximum cap on repair costs, provided the total loan amount falls within local FHA loan limits.

Not sure if an FHA product is the best fit? You might also want to compare these options against a conventional renovation loan to ensure you secure the most favorable terms for your specific financial situation.

| Feature | Limited FHA 203(k) | Standard FHA 203(k) |

|---|---|---|

| Maximum Repair Amount | Up to $35,000 | No limit (subject to FHA max loan limits) |

| Minimum Repair Amount | None | $5,000 |

| Structural Repairs Allowed? | No | Yes |

| HUD Consultant Required? | No | Yes |

| Best For | Cosmetic updates, appliances, flooring | Major additions, foundation work, full remodels |

Why Choose The Tyler Osby Team for Your FHA 203k Renovation?

Navigating the complexities of an FHA 203k loan requires a knowledgeable mortgage broker. At The Tyler Osby Team, we pride ourselves on being the most recommended mortgage lender in Iowa. We understand the Urbandale real estate market and have the expertise to guide you through every step of the renovation loan process.

Did another lender deny your renovation project? We are experts at providing second opinions on FHA 203k renovation loans. We often find solutions where others see roadblocks. Our team provides weekly updates so you always know exactly where your application stands from start to finish.

Legal Licensing Information: Fairway Independent Mortgage Corporation, NMLS #2289. Tyler Osby, NMLS #8668, State of Iowa License #19545.

Q1: What is the minimum credit score required for an FHA 203k loan?

Typically, you need a minimum credit score of 580 to qualify for the maximum financing of an FHA 203k loan, though higher scores may offer better terms and lower interest rates.

Q2: Can I do the renovation work myself?

No, FHA guidelines require that all renovation work be completed by licensed and insured general contractors. Self-help repairs are generally not permitted to ensure the work meets professional standards.

Q3: Is the FHA 203k loan available for investment properties?

No, the FHA 203k loan is strictly for primary residences. You must intend to live in the home you are renovating, though it can be used for multi-unit properties up to four units if you live in one of them.

Q4: How long do I have to complete the renovations?

Contractors typically have up to six months to complete the approved renovations after the loan closes, depending on the scope and complexity of the project.

Q5: Can I use an FHA 203k loan to refinance my current home?

Yes! If you already own a home in Urbandale that needs significant repairs, you can use an FHA 203k refinance to fund those home improvements without taking out a separate personal loan.Apply Online with The Tyler Osby Team Today